Learn About Social Security's Online Tools

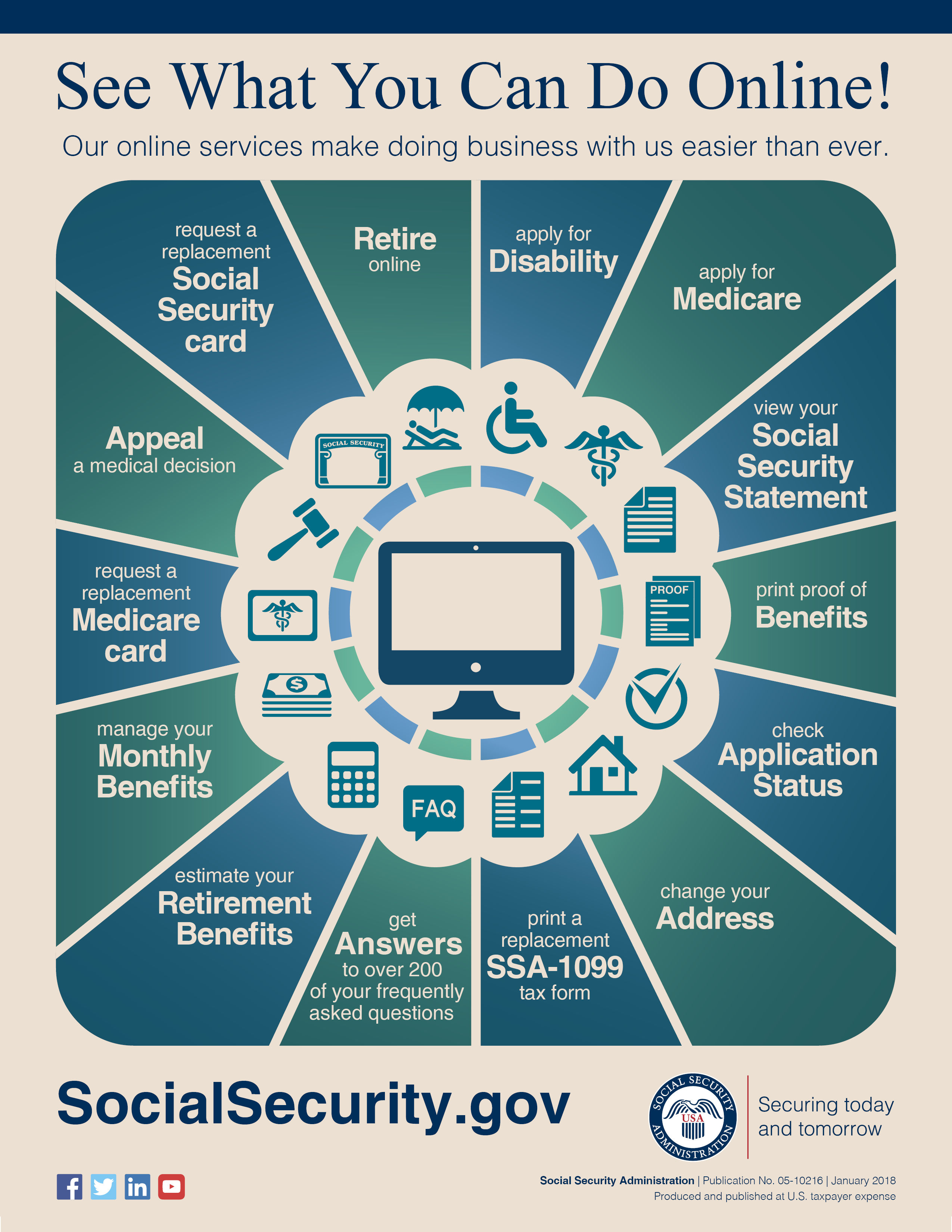

With the aging population becoming increasingly tech savvy, the Social Security Administration (SSA) has moved a lot of services online. From applying for Social Security benefits to replacing a card, the SSA has online tools to help.

With the aging population becoming increasingly tech savvy, the Social Security Administration (SSA) has moved a lot of services online. From applying for Social Security benefits to replacing a card, the SSA has online tools to help.

To access most of the online services, you need to create a mySocial Security account. This account allows you to receive personalized estimates of future benefits based on your real earnings, see your latest statement, and review your earnings history. You can also request a replacement Social Security card, check the status of an application, get direct deposit, or change your address. If you are a representative payee, you can use my Social Security to complete representative payee accounting reports. Even if you don't get benefits, you can use the account to request a benefit verification letter.

In addition to my Social Security, other online services are available, including the following:

- Apply for retirement, Medicare, and disability benefits

- Apply for Supplemental Security Income in some circumstances

- Appeal a medical decision or a non-medical decision

- Find out what benefits you qualify for

- Estimate future benefits

- Find your full retirement age

- Block electronic access to your Social Security information

The Internal Revenue Service (IRS) is increasing the amount taxpayers can deduct from their 2019 income as a result of buying long-term care insurance.

The Internal Revenue Service (IRS) is increasing the amount taxpayers can deduct from their 2019 income as a result of buying long-term care insurance. A power of attorney is one of the most important estate planning documents, but when one sibling is named in a power of attorney, there is the potential for disputes with other siblings. No matter which side you are on, it is important to know your rights and limitations.

A power of attorney is one of the most important estate planning documents, but when one sibling is named in a power of attorney, there is the potential for disputes with other siblings. No matter which side you are on, it is important to know your rights and limitations.